If you’ve ever looked at a company’s balance sheet and wondered what “additional paid-in capital” means, you’re not alone. I remember the first time I saw it, it sounded more complicated than it really is.

In this guide, I’ll break down what additional paid-in capital is in plain terms so you can finally understand it without the accounting jargon. You’ll learn what it means, how it’s calculated, and why it matters for both investors and businesses.

By the end, you’ll know exactly how to spot it on a financial statement and what it tells you about a company’s financial strength.

What is Additional Paid-In Capital (APIC)?

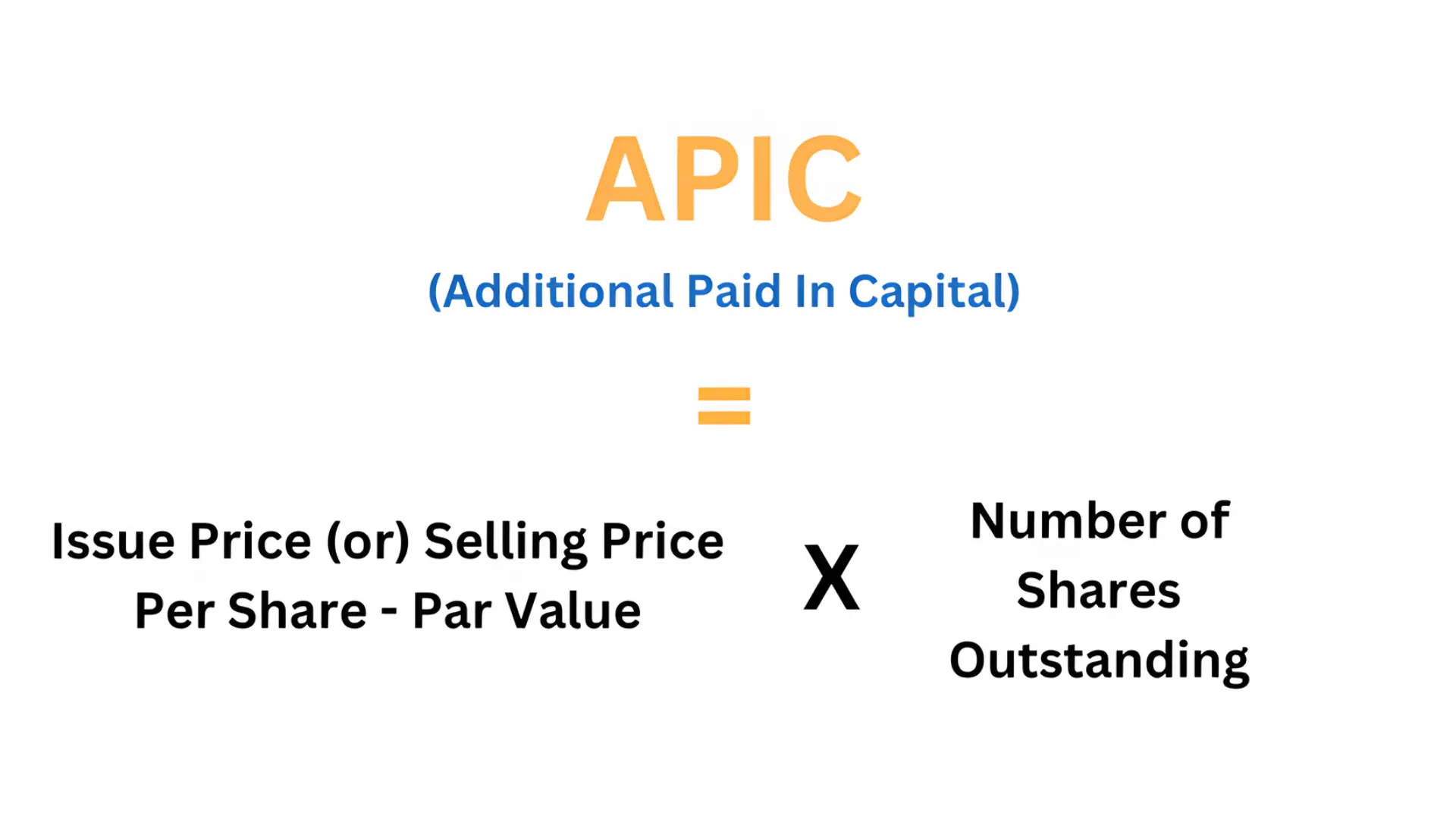

Additional paid-in capital (APIC) is the amount investors pay above the par value of a company’s stock when they buy shares.

For example, if a company sells stock with a $1 par value but investors pay $10 per share, the extra $9 per share is recorded as additional paid-in capital. This isn’t revenue or profit. It’s part of the total money investors contribute to help the company grow.

You can calculate APIC with this formula:

APIC = (Issue Price minus Par Value) x Number of Shares

Here’s what each part means:

- Issue Price: The price investors pay per share.

- Par Value: The base or face value of each share.

- Number of Shares: The total shares sold.

Example: If a company issues 1,000 shares at $12 each and the par value is $1:

= (12 minus 1) x 1,000 = $11,000

That $11,000 becomes additional paid-in capital.

If the company pays fees or commissions to issue shares, those costs are subtracted from APIC because they reduce the total amount raised. This is one of the first concepts worth understanding if you’re exploring investing for beginners and trying to make sense of what companies do with shareholder money.

How APIC Appears on Financial Statements

You’ll find APIC under shareholders’ equity on the balance sheet, usually listed below “Common Stock” or “Preferred Stock.”

On the cash flow statement, stock sales appear under financing activities, while APIC itself stays in the equity section. APIC doesn’t show up on the income statement because it’s not revenue. It’s part of the money investors contribute, not income from business operations.

Journal Entries for Additional Paid-In Capital

When a company issues stock above par value, the journal entry separates the par value and APIC.

Example:

| Account | Debit | Credit |

|---|---|---|

| Cash | $10,000 | |

| Common Stock ($1 par x 1,000 shares) | $1,000 | |

| Additional Paid-In Capital | $9,000 |

If the company pays issuance costs, they’re deducted from APIC. Preferred stock follows the same rule: any amount received above par goes to Additional Paid-In Capital — Preferred.

Components of Paid-In Capital

Paid-in capital has two main parts:

- Par Value (Share Capital): The legal face value of issued shares.

- Additional Paid-In Capital: The extra amount paid above par.

Example: If 2,000 shares are sold at $8 each with a $1 par value:

- Common Stock = $2,000

- APIC = $14,000

- Total Paid-In Capital = $16,000

This split shows how total capital is split between par value and the amount investors actually paid. It’s a useful number to track alongside the debt-to-equity ratio, which shows how much of a company’s financing comes from debt versus shareholder contributions.

APIC vs. Other Equity Accounts

It’s easy to mix up additional paid-in capital with other equity accounts since they all sit in the same section of the balance sheet. Here’s a simple comparison:

| Comparison | Description |

|---|---|

| APIC vs. Par Value | Par value is the minimum legal value per share. APIC is the extra amount investors pay above that value. |

| APIC vs. Retained Earnings | APIC comes from money that investors contribute. Retained earnings come from company profits that stay in the business. |

| APIC vs. Contributed Capital | Contributed capital is the total amount shareholders have invested, which includes both par value and APIC. |

| APIC vs. Share Premium | In many countries outside the U.S., APIC is called “share premium.” Both terms mean the same thing: money paid above par value. |

Separating these accounts helps you understand how each one contributes to a company’s overall equity. The distinction becomes even clearer when you look at how retained earnings work in income-generating businesses, where profits accumulate separately from what shareholders originally paid in.

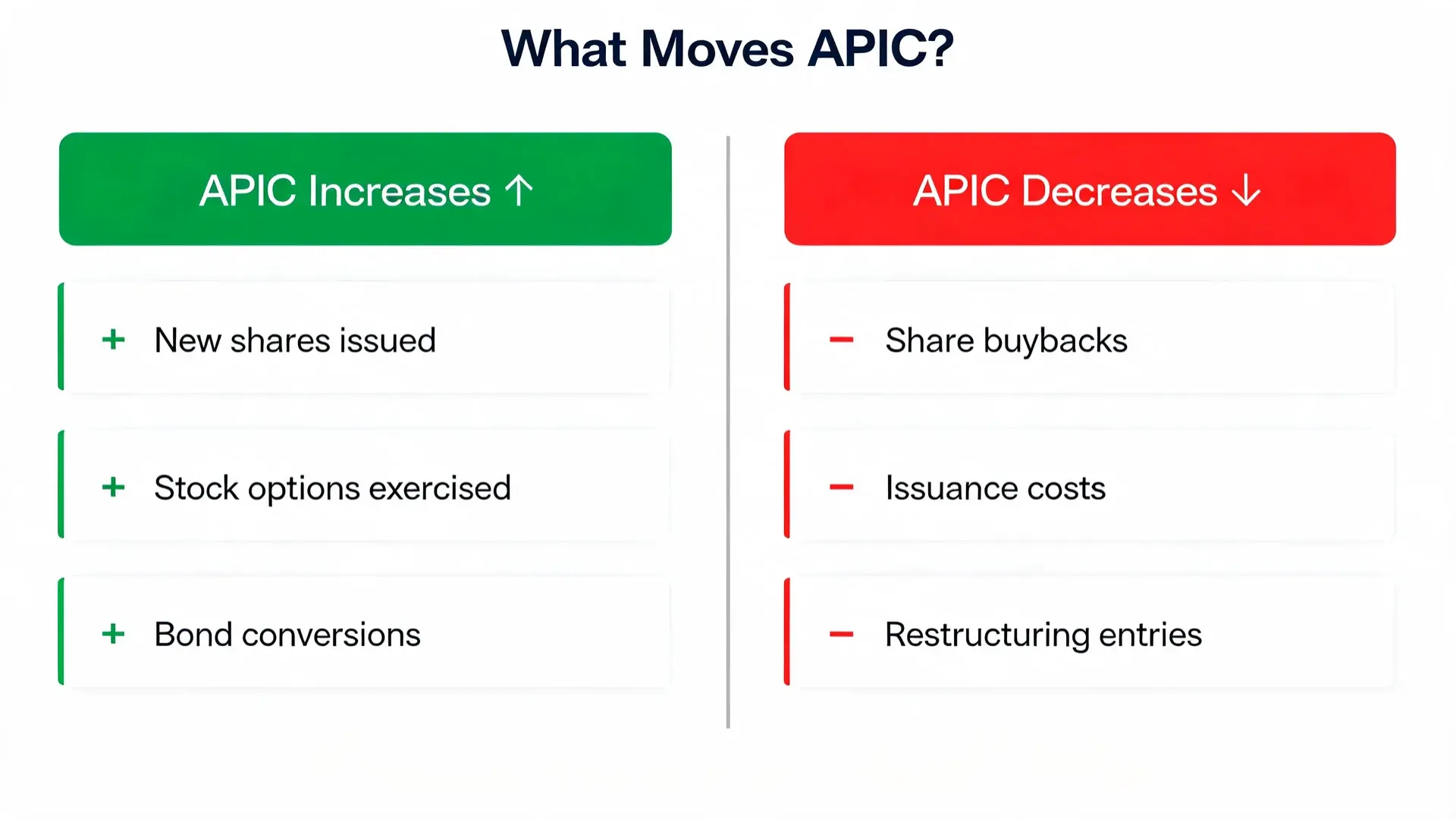

Factors That Increase or Decrease APIC

A company’s additional paid-in capital doesn’t stay the same forever. It changes when the company issues, repurchases, or adjusts its shares. These movements reflect how investors interact with the company through equity transactions rather than day-to-day business activity.

APIC Increases When

- The company issues new shares above par value

- Employees exercise stock options or warrants

- Bonds or preferred shares convert to common stock

APIC Decreases When

- The company buys back its shares

- Stock issuance costs are recorded

- Certain restructuring entries adjust equity

APIC only changes through equity-related actions. It’s not affected by operating profits, losses, or normal business expenses.

Only events tied to ownership and capital structure move the number. This is also why reading the equity section matters when comparing stocks and bonds, since net income alone doesn’t tell the full story.

Examples of Additional Paid-In Capital

To see how additional paid-in capital works in practice, here are three real-world situations where APIC increases when shares are issued above par value.

1. IPO Example

When a company goes public, it sells stock to investors for the first time. If the stock price is $25 per share and the par value is $0.01, the extra $24.99 per share becomes APIC. That gap shows how much investor confidence the company has built before a single share traded on the open market.

2. Private Investment

Private investors can also add to APIC. If they buy shares at $5 each with a $1 par value, the extra $4 per share is recorded as additional paid-in capital. This type of investment strengthens the company’s balance sheet without adding debt.

3. Employee Stock Options

When employees exercise stock options, they buy shares directly from the company, often at a set price. If the exercise price is higher than par value, that difference adds to APIC. It benefits both the employees and the company by boosting ownership and equity without any cash changing hands externally.

Each of these cases increases shareholders’ equity without affecting the company’s net income. APIC grows through investment activity, not from day-to-day operations.

Why Additional Paid-In Capital Matters

APIC shows how much confidence investors have in a company. When investors pay more than the par value, they’re saying the company is worth more than its base share price. That premium also feeds into how analysts calculate enterprise value, which lenders and acquirers use when sizing up a business.

Common Mistakes and Misunderstandings to Avoid

Even experienced bookkeepers make small errors when recording additional paid-in capital. These mistakes can change how equity looks on the balance sheet, so it’s worth knowing the most common ones:

- Recording all proceeds under common stock: Always separate the par value from APIC. Only the par value portion belongs under “common stock.”

- Forgetting to deduct issuance costs: Expenses like legal or underwriting fees should be subtracted from APIC, not ignored or recorded as regular expenses.

- Treating APIC as income: APIC comes from investors, not business operations. It should never appear on the income statement.

Keeping these entries correct helps your financial statements stay accurate and gives a clearer picture of where your company’s equity comes from. The same care applies to other balance sheet items, like how the double declining balance method affects asset values over time.

Frequently Asked Questions About Additional Paid-In Capital

Can additional paid-in capital be negative?

APIC can technically be reduced to zero or become negative in certain situations, though it’s uncommon. This can happen when a company repurchases shares at a price higher than the original purchase price, and the excess is charged against APIC after retained earnings are exhausted.

Some restructuring or recapitalization transactions can also reduce APIC significantly. If it goes negative, it’s usually a sign of aggressive buyback activity or unusual accounting adjustments worth investigating further.

Does additional paid-in capital affect net income?

No, APIC has no effect on net income. Because it comes from share issuances rather than business operations, it doesn’t flow through the income statement at all. Net income is driven by revenue, expenses, and taxes from the company’s core activities.

APIC only appears on the balance sheet as part of shareholders’ equity. This is one of the reasons investors look at both the income statement and the equity section separately when evaluating a company’s financial health.

How does a stock buyback affect additional paid-in capital?

When a company repurchases its own shares, the transaction is recorded as treasury stock, which reduces total shareholders’ equity.

If the company retires those shares, the original par value and APIC associated with them are removed from the books.

If the repurchase price exceeds the original issue price, the difference is charged first to retained earnings and then to APIC if retained earnings run out. This is why heavy buyback programs can sometimes reduce or eliminate APIC over time.

Summing Up

Now that you know what additional paid-in capital means, you can look at a company’s financial statements with more clarity. You’ve learned what it is, how to calculate it, and why it matters when reading the equity section of a balance sheet.

I see APIC as a straightforward reflection of investor trust. It shows how much people are willing to pay above a stock’s base value, and that tells you something real about confidence in the business.

Keep this in mind the next time you review a balance sheet, and check out my other finance blogs for more clear, practical breakdowns like this one.