If you’re trying to stop the cycle of making financial decisions you later regret, the problem usually isn’t willpower or math. It’s alignment.

Your spending, saving, and giving habits are either pulling toward what you actually care about or quietly working against it. That gap is what financial values are designed to close.

This guide explains what financial values are, how they differ from financial goals, and how to use them as a practical filter for every money decision you face, from setting up a budget to deciding how to invest.

✅ Key Takeaways:

|

| ⚠️ Disclaimer: This article is for educational purposes only and does not constitute financial or investment advice. Always consult a qualified financial advisor before making investment decisions. |

What are Financial Values?

Financial values are the core beliefs that shape how you relate to money. They’re not the same as your financial goals.

A goal is the destination, like paying off $12,000 in credit card debt. Your financial values are the reason that destination matters to you in the first place, whether that’s freedom from obligation, security for your family, or the ability to make choices without debt dictating the answer.

The Consumer Financial Protection Bureau defines financial well-being as having the security and freedom of choice to make decisions that let you enjoy life. Your financial values determine what “enjoying life” actually looks like for you.

Everyone has financial values, even people who have never named them. The difference is whether you’re acting on values you’ve consciously chosen or ones you’ve unconsciously absorbed from family, culture, or social pressure.

Financial Values vs. Financial Goals: What’s the Difference?

Most people know what their financial goals are. Fewer know what their financial values are. The distinction matters because goals without underlying values tend to collapse when the going gets hard.

| Financial Values | Financial Goals |

| The “why” behind money decisions | The “what” you’re working toward |

| Ongoing and stable over time | Time-bound and achievable |

| Example: Security | Example: Save $15,000 emergency fund by December |

| Example: Freedom | Example: Pay off student loans within 3 years |

| Example: Family | Example: Fund a 529 college savings plan for two kids |

When a goal connects to a value, it gains staying power. When it doesn’t, it’s easy to abandon the moment it becomes inconvenient.

Common Financial Values and What They Look Like in Practice

Most financial values fall into a handful of categories. Understanding which ones resonate for you is more useful than trying to adopt values that sound admirable but don’t actually reflect how you think about money.

Security means feeling most comfortable with buffers in place. If security is a top value, a six-month emergency fund probably matters more to you than maximizing returns. You’d rather know the money is there than chase an extra 2% yield.

Freedom shows up as a strong aversion to financial obligation. For example, someone who values freedom above security might aggressively pay off their mortgage early, not because it’s the mathematically optimal move, but because being debt-free is what freedom means to them.

Generosity means giving is part of your financial plan, not an afterthought. This could be charitable giving, covering family members’ expenses, or supporting causes that align with your beliefs. Research from the Federal Reserve’s Report on the Economic Well-Being of U.S. Households shows that financial resilience and charitable behavior are correlated, suggesting that people with clearer financial priorities are better positioned to give.

Family means financial decisions are evaluated first through the lens of household stability. College savings, life insurance, and estate planning tend to be priorities here even when they’re not the most exciting topics.

Growth looks like continuous investment in yourself or your money. Someone who values growth finds it easy to spend on professional development, index funds, or business ideas, but feels guilty about spending the same amount on a vacation that doesn’t seem “productive.”

Simplicity means low complexity. Someone who values simplicity might prefer a single, all-in-one fund to managing a multi-account portfolio, even if a more complex setup would theoretically yield better outcomes. The reduced cognitive load is worth the trade-off.

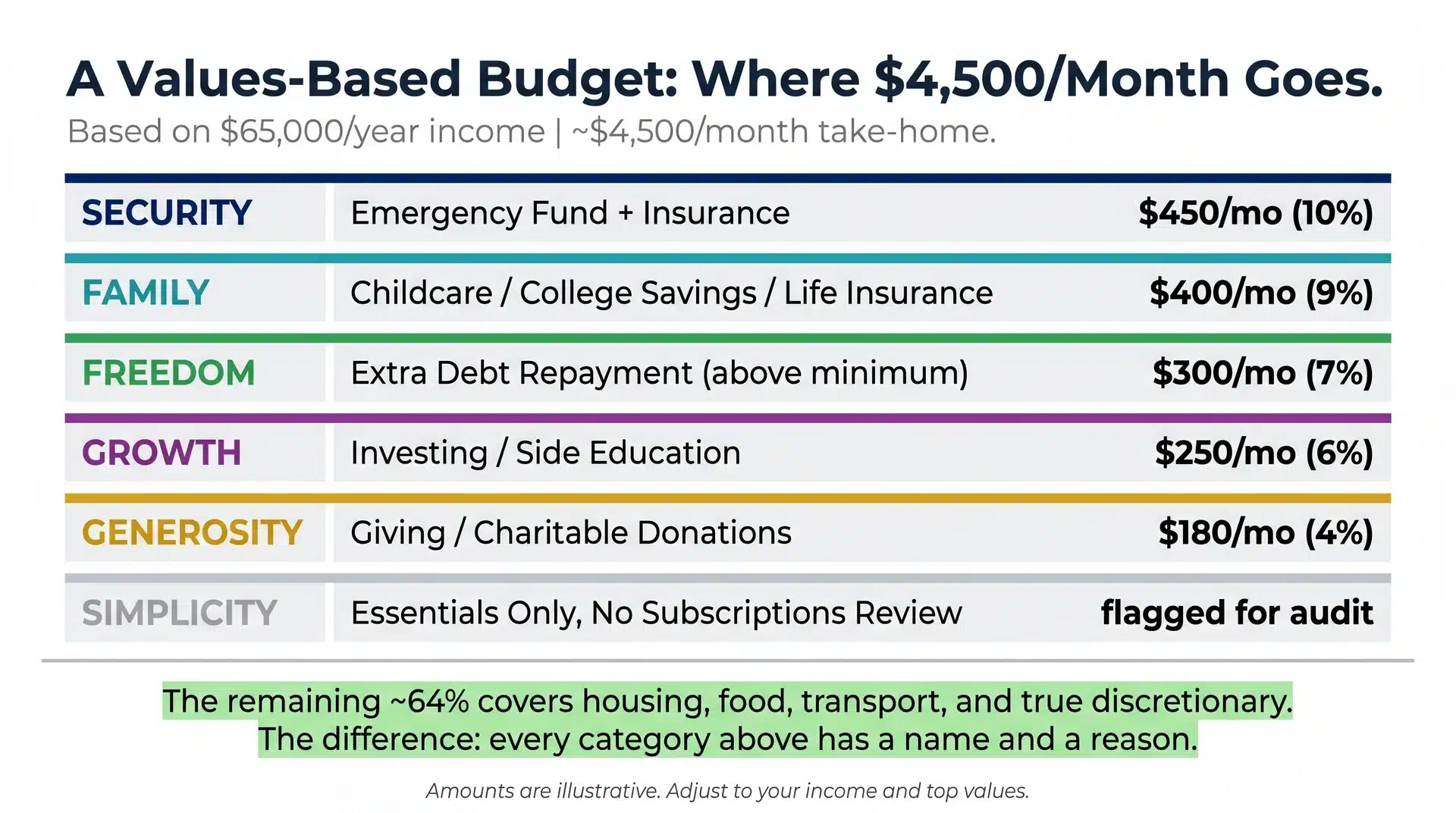

Why Financial Values Matter to Your Budget and Decision-Making

A budget built around categories alone, rent, groceries, and subscriptions rarely holds up over time because the categories don’t explain why any particular number matters. A values-based budget changes that. It ties each spending area to something you actually care about, which makes it much easier to see in real time when your money is working against you.

Here’s a concrete example:

Suppose you earn $65,000 per year and take home roughly $4,500 per month after taxes and benefits. If security is one of your top values, your budget might allocate $450 per month (10% of take-home) to building an emergency fund. That’s not an arbitrary savings rate; it’s a direct expression of a value you’ve named. On a night when you’re tempted to book a last-minute trip instead, you have a real reason to say no, one that’s rooted in something you care about rather than guilt or willpower.

If you haven’t yet built a structured budget, connecting values to specific line items is one of the most effective ways to make that process stick.

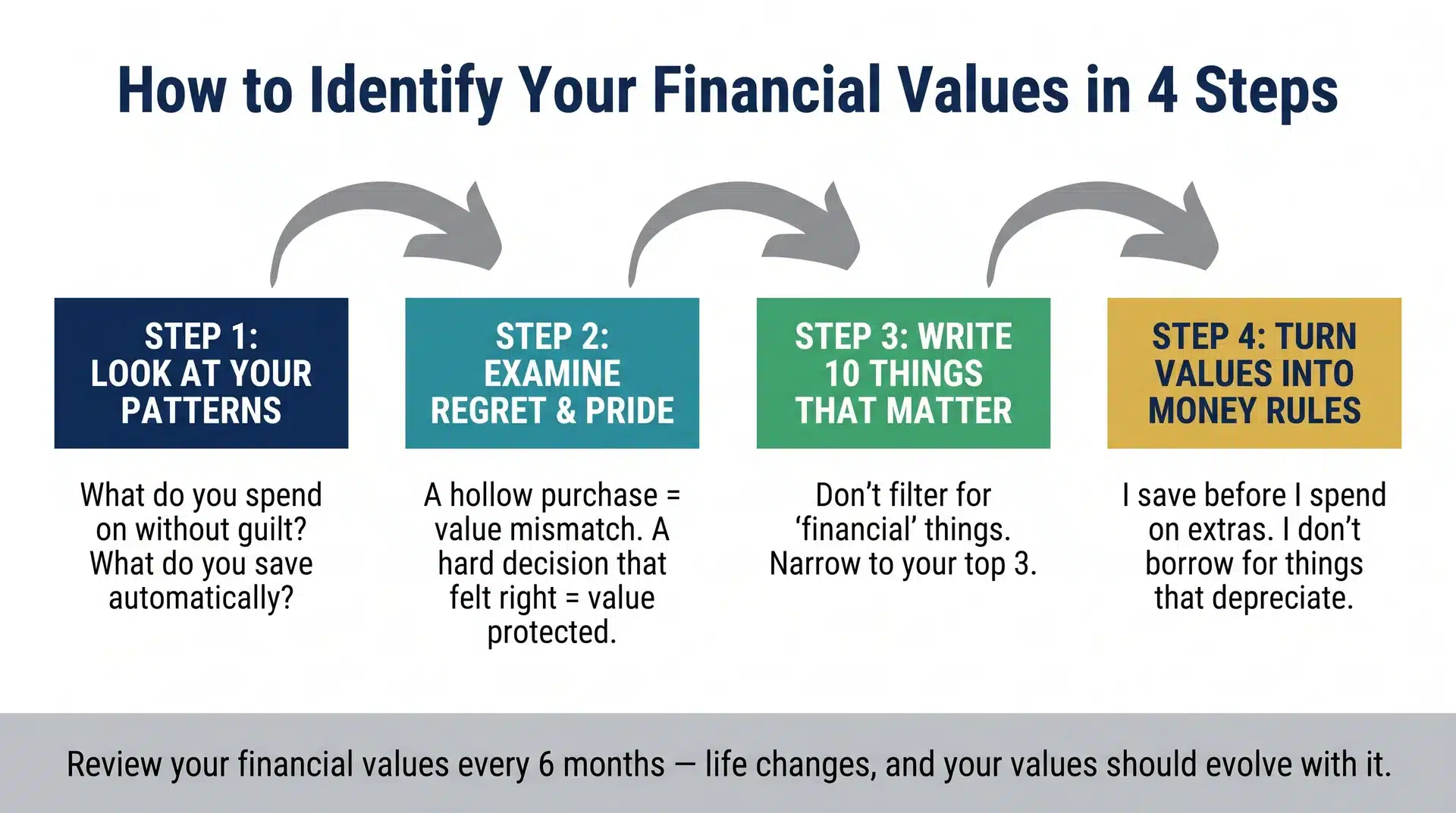

How to Identify Your Financial Values

Most people haven’t formally identified their financial values, which is why spending decisions often feel reactive rather than intentional. Here’s a straightforward process to get clear on yours.

Step 1: Look at where money goes without debate. What do you spend on without guilt or hesitation? What do you save for automatically, without being asked? These patterns reveal values already in action.

Step 2: Examine money decisions that caused conflict or regret. A purchase that feels hollow afterward usually means the money went toward something that doesn’t align with a value. A decision you agonized over and then felt great about usually means a value was at stake.

Step 3: Write down ten things that matter most to you. Don’t filter for “financial” things. Security, adventure, family time, creative work, and health are all valid. Then narrow to your top three. These are your financial values for now, understanding they may shift as your life changes.

Step 4: Turn each value into a short money rule. “I save before I spend on extras.” “I give 5% of every paycheck.” “I don’t take on debt for things that depreciate.” These rules don’t require motivation to follow because they’re connected to something you already believe.

What Happens When Financial Behaviors and Values Don’t Align

Financial stress often isn’t caused by a lack of income. It’s caused by a consistent mismatch between how money actually moves and what a person says matters to them.

Someone who values security but carries high-interest credit card debt month to month will feel that tension even when they can technically cover the minimum payments. The behavior is actively working against the value.

A 2023 Federal Reserve survey found that 35% of adults said they would struggle to cover a $400 emergency expense using savings alone. That statistic is frequently interpreted as a spending problem, but it’s often a values-alignment problem.

The people in that group aren’t necessarily overspending frivolously; many have never explicitly decided that emergency reserves matter enough to protect before other spending.

Naming your values doesn’t automatically close the gap, but it does make the gap visible. Once you see it, adjusting becomes a practical exercise rather than a willpower contest.

How Financial Values, Mindset, and Goals Connect

Values sit at the foundation. They shape your financial mindset, which is how you talk to yourself about money.

Things like whether you believe you’re capable of building wealth, whether you think of spending as a reward or a risk, and whether debt feels like a tool or a trap.

Your mindset, in turn, determines which goals feel worth pursuing and which feel pointless.

When the three are aligned, financial decisions become genuinely easier. Not because the math is simpler, but because every choice has a clear answer: does this move me toward what I’ve said matters, or away from it?

How to Apply Financial Values to Budgeting and Spending

Values-based budgeting works by labeling every budget category with the value it serves. Rent and utilities serve security. A travel fund serves freedom or experience. A 529 contribution serves the family. Charitable giving serves generosity.

When you review spending at the end of the month, the question changes. Instead of “did I overspend?”, you’re asking “did this spending reflect what I said mattered to me?” That’s a much more useful question, because it surfaces specific decisions rather than abstract totals.

A few practical moves to implement this:

- Automate savings that reflect your top values first. If security matters, set up automatic transfers to your emergency fund on payday before any discretionary spending happens.

- Add a 24-hour rule for non-essential purchases above $50. That pause exists specifically to ask whether the purchase aligns with a named value.

- Review your actual spending against your values every 90 days, not just against your budget categories. If generous giving is a value, but zero dollars were given to it this quarter, that’s the data you need.

Sharing and Aligning Values with a Partner or Family

Money conflicts in relationships almost always come down to value disagreements, not income or budget numbers.

One partner values security and wants to build reserves; the other values experience and wants to take the trip now.

Neither is wrong. But without a shared language for what each person actually cares about, every money conversation becomes a negotiation without a framework.

A straightforward starting point: both partners write down their top three financial values independently, then compare.

Look for overlap first. If both lists include “family” and “security,” that’s common ground to build joint goals on.

Address the gaps directly, without judgment. The goal isn’t to force agreement; it’s to understand what each person is actually protecting when they argue for a particular financial decision.

When to Review and Update Your Financial Values

Financial values are stable but not permanent. A 28-year-old single professional and a 41-year-old with two kids and a mortgage have legitimately different financial values, and that’s appropriate.

Life changes, including marriage, children, job transitions, health events, and retirement, often shift which values carry the most weight.

A useful rhythm is a brief values review every six months, separate from your regular budget review.

Ask three questions:

- Are my current financial behaviors serving what I actually care about?

- Has anything changed in my life that should shift my priorities?

- Are my goals still aligned with the values I hold, or have the values shifted?

Adjusting is not failure. It’s the process working correctly.

Common Mistakes to Avoid

Adopting values that sound aspirational but aren’t actually yours. If you write down “generosity” because it sounds noble, but you rarely think about giving when you make financial decisions, it won’t function as a real filter. Values only work when they reflect how you actually think, not how you’d like to be seen.

Setting goals without tracing them to a value. A savings goal with no underlying value tends to collapse under any real pressure. Before committing to a financial goal, be able to answer: which value does this serve?

Letting values calcify when life changes. Treating your 20s financial values as permanent is a common mistake. A value like “freedom,” which meant “travel and flexibility” at 25, might need to be reframed as “financial independence” at 45. The underlying belief is similar; the way it’s expressed needs to evolve.

Ignoring the emotion embedded in money decisions. Fear, guilt, and status-seeking are all value signals. A purchase driven by anxiety is often a misguided attempt to satisfy a security value. Recognizing the emotion doesn’t mean acting on it; it means understanding the need that drives the impulse.

Frequently Asked Questions

What are financial values?

Financial values are the personal beliefs and priorities that guide how you earn, spend, save, and give money. They’re the underlying “why” behind your financial behavior, things like valuing security, freedom from debt, family stability, or the ability to give generously.

What are some examples of financial values?

Common examples include security (building financial buffers and emergency savings), freedom (avoiding debt and maintaining flexibility), generosity (giving to family or charitable causes), growth (investing consistently in yourself or your money), simplicity (keeping finances easy to manage), and family (prioritizing the financial stability of your household).

Why are financial values important?

Financial values provide a stable framework for your money decisions that doesn’t require constant motivation to maintain. When your spending and saving align with your actual values, financial choices feel clearer and less stressful. When they don’t, even an adequate income can produce persistent financial anxiety.

How do you identify your personal financial values?

Start by examining your existing patterns: what do you spend on without hesitation, and what do you save for automatically? These are likely already reflecting values in action. Then look at decisions you’ve regretted, because regret usually signals a conflict between behavior and value. Write down 10 things that matter to you, narrow them to your top three, and translate each into a short money rule that guides day-to-day decisions.

How do financial values affect budgeting?

Values-based budgeting labels every spending category with the value it serves: security, family, growth, experience, and so on. This shifts your monthly budget review from “did I stay within the numbers?” to “did my money go toward what I said mattered?” The second question is far more actionable because it identifies specific decisions rather than abstract totals. It also makes it easier to cut spending in categories that don’t serve any named value.

What is the difference between personal values and financial values?

Personal values are the broader beliefs that guide how you live, such as honesty, creativity, community, and ambition. Financial values are the subset of those beliefs that specifically shape how you relate to money. They often overlap. Identifying where your broader values intersect with money decisions is one of the most direct paths to understanding your financial values.

The Real-Money Move: Start with One Value, Not Three

Most people who try to build a values-based financial plan attempt to work with all their values at once and stall out within a week.

The approach that actually works is simpler. Pick the one financial value that causes the most friction in your current money life, the one where the gap between what you say matters and what your bank statement shows is the widest.

For most people, that’s either security (they want a cushion but keep spending before saving) or freedom (they resent debt but keep adding to it).

Once you’ve named that one value, do exactly one thing this week to act on it. If it’s security, set up an automatic transfer of $100 from your checking account to a separate savings account to land on your next payday.

If it’s about freedom, calculate the exact payoff date for your highest-interest debt and post it somewhere visible.

A single concrete action tied to a named value does more for long-term financial behavior than a full budget overhaul you’ll abandon by month two.

The other values don’t disappear. Once the first one is anchored in a real habit, you add the second. That’s how a values-based financial plan actually gets built, one real-money decision at a time.