Most business owners focus on revenue and expenses but overlook one of the simplest legal ways to reduce taxable income – choosing the right depreciation method.

If you bought a vehicle, computer, or piece of equipment this year, the double-declining balance method can let you write off a much larger share of that cost upfront than the default approach. That means a lower tax bill now, not spread across five years.

This guide explains exactly how the double-declining balance method works, when to use it, what the IRS says about it, and how to calculate it step by step with a real-dollar example.

| ⚠️ Disclaimer: This article is for educational purposes only and does not constitute financial or investment advice. Tax rules vary by situation and change over time. Always consult a qualified tax professional or CPA before making depreciation decisions for your business. |

✅ Key Takeaways:

|

What is the Double Declining Balance Method?

The double-declining balance method is an accelerated depreciation technique that applies twice the straight-line rate to an asset’s declining book value each year.

Because the depreciation rate remains fixed while the asset’s book value shrinks annually, the amount you deduct each year decreases.

The result is you capture most of the asset’s total depreciation in the first two or three years of ownership, when the asset is newest, most valuable, and generating the most income for your business.

Think of it this way. A laptop you buy today for $2,000 is not worth $1,600 next year and $1,200 the year after in any realistic sense. It will lose a large portion of its value in the first year simply because it is no longer new.

The double declining balance method matches your deductions to that real-world pattern, rather than pretending the laptop depreciates at a flat $200 per year for 10 years.

The Double Declining Balance Method Formula

The core depreciation formula is straightforward once you understand its two moving parts. The rate is fixed. The base it applies to changes every year.

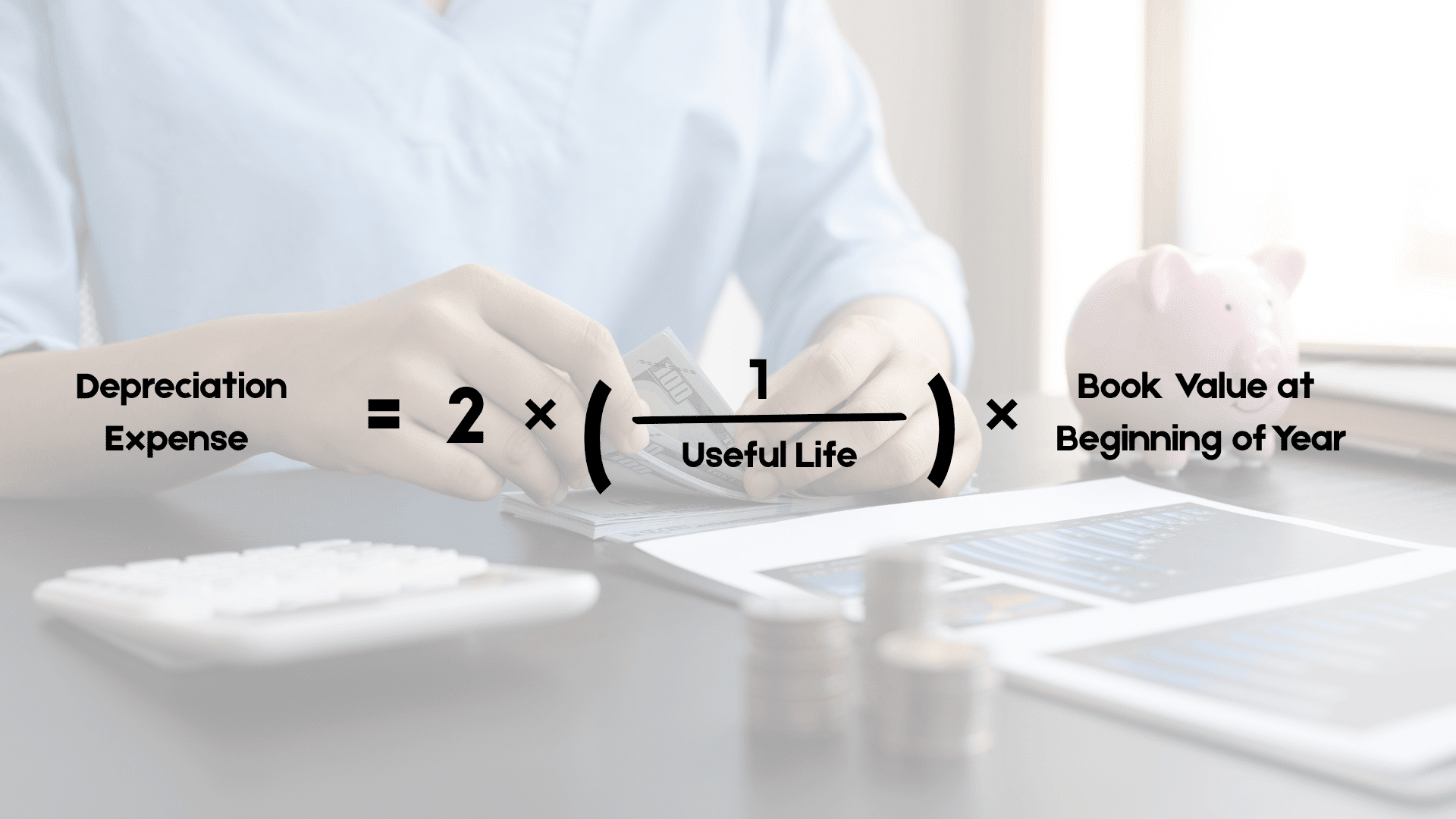

Depreciation Expense = Beginning Book Value x (2 / Useful Life in Years)

Before you calculate, you need four numbers. Here is what each one means and where to find it:

| Component | What It Is | Where to Find It |

|---|---|---|

| Asset Cost | The total amount you paid to acquire and prepare the asset for use | Purchase receipt, invoice, or closing documents |

| Useful Life | How many years the asset is expected to generate value | IRS Publication 946 tables or manufacturer guidance |

| Salvage Value | The estimated resale or scrap value at the end of the asset’s life | Market research or accounting judgment |

| Beginning Book Value | The asset’s original cost minus all depreciation taken so far | Your balance sheet or depreciation schedule |

The depreciation rate is always 2 divided by the useful life. For a 5-year asset, that is 40%. For a 7-year asset, it is roughly 28.6%. This rate stays the same every year. What changes is the book value you apply it to.

How to Calculate Double Declining Balance Depreciation: A Step-by-Step Example

Here is a full depreciation schedule for a common business scenario. Imagine you purchase a delivery van for your small business for $10,000.

The IRS assigns vehicles like this a 5-year useful life under MACRS. You estimate the van will be worth $1,000 as a trade-in after five years.

Asset Details:

- Purchase Price: $10,000

- Useful Life: 5 years

- Salvage Value: $1,000

- Depreciation Rate: 40% (2 divided by 5 years)

| Year | Beginning Book Value | Depreciation Rate | Depreciation Expense | Ending Book Value |

|---|---|---|---|---|

| 1 | $10,000 | 40% | $4,000 | $6,000 |

| 2 | $6,000 | 40% | $2,400 | $3,600 |

| 3 | $3,600 | 40% | $1,440 | $2,160 |

| 4 | $2,160 | 40% | $864 | $1,296 |

| 5 | $1,296 | Adjusted | $296 | $1,000 |

Notice that you deduct $6,400 in the first two years alone. With straight-line depreciation on the same van, you would deduct only $3,600 over those same two years.

That $2,800 difference represents taxable income you are deferring to later years, freeing up real cash now.

The final year requires an adjustment. The formula would produce $518 (40% of $1,296), but that would bring the book value below the $1,000 salvage value.

You cap the deduction at $296, so the ending book value equals the salvage value.

Double Declining Balance vs. Straight-Line Depreciation: Which One is Right for Your Business?

The right choice depends on the type of asset you are depreciating and your cash flow priorities. Here is how the two methods compare on every factor that matters for a real-money decision:

| Factor | Straight-Line Method | Double Declining Balance Method |

|---|---|---|

| Depreciation Pattern | Equal expense every year | Higher early-year expense, lower later |

| Annual Deduction | Same amount each year | Decreases each year |

| Calculation Basis | (Cost minus Salvage Value) divided by Useful Life | Book Value x (2 divided by Useful Life) |

| Tax Benefit Timing | Spread evenly across the useful life | Front-loaded in the first two to three years |

| Best For | Buildings, office furniture, stable-use assets | Vehicles, computers, heavy machinery, technology |

| Complexity | Simple, consistent | Recalculated annually |

| Impact on Net Income | Steady, predictable reduction | Larger reduction early, smaller later |

| Impact on Investors | Smooth earnings profile | Lower reported earnings in the early years |

The lower reported earnings in the early years are worth flagging. If you are seeking outside investment or applying for a loan, your debt-to-equity ratio and profitability metrics may look less favorable in years one and two under DDB.

That is not an accounting error. It is a feature of accelerated depreciation. Investors who understand financial statements will see through it. Lenders may not, so consider the context before committing to this method.

When Does the Double Declining Balance Method Make Sense for Your Business?

Use the double declining balance method when the asset genuinely loses most of its value in its first few years. The deduction pattern should match the actual economic reality of the asset.

Vehicles are the clearest case. A $35,000 work truck loses roughly 20% of its value the moment it leaves the lot and another 15% in year two, according to typical automotive depreciation curves. Claiming 40% of its cost as a deduction in year one reflects what is actually happening to the asset’s value.

Computers and technology equipment follow the same logic. A server rack that costs $15,000 today may be functionally obsolete in three years as newer, faster hardware replaces it.

Software development firms, IT companies, and any business that depends on hardware cycles benefit from expensing that equipment aggressively upfront.

Heavy machinery for manufacturing and construction also qualifies. Equipment that runs at full capacity during its first years and requires more maintenance later should be depreciated faster in the early, high-productivity period.

Where this method does not apply: buildings, land improvements, office furniture, and any asset that provides consistent value year after year with minimal obsolescence. Those assets belong on a straight-line schedule. Applying DDB to a commercial property is not only inaccurate but can also create compliance issues under GAAP reporting requirements.

How the IRS Handles Accelerated Depreciation: What You Need to Know About MACRS

Here is where the double declining balance method becomes directly relevant to your tax return. According to IRS Publication 946, the Modified Accelerated Cost Recovery System (MACRS) is the method most U.S. businesses are required to use for tax depreciation on assets placed in service after 1986. MACRS uses double-declining balance as its standard depreciation method for the most common asset categories.

For 3-year, 5-year, 7-year, and 10-year property classes (which cover most business vehicles, computers, and equipment), MACRS defaults to the 200% declining balance method. That is exactly DDB.

The system automatically switches to straight-line depreciation in the year it produces a larger deduction, thereby maximizing your write-off over the asset’s full life.

If you depreciate business assets on your tax return, you are already using a version of double declining balance, whether you know it or not. Understanding the mechanics gives you better insight into your depreciation schedule and helps you catch errors before they become problems during an IRS review.

Section 179 expensing and bonus depreciation rules can allow you to deduct the entire cost of eligible assets in year one, going further than even DDB allows.

These are separate elections with their own rules and limits. Your CPA can determine whether they apply to your situation. The point is that the IRS framework favors front-loaded deductions for most business assets, which is exactly what DDB delivers.

Double Declining Balance Method: Advantages & Disadvantages

| Advantages | Disadvantages |

|---|---|

| Reduces taxable income significantly in early years, keeping more cash in the business when the asset is newest and most productive | Requires annual recalculation because the base changes every year, unlike the straight-line which uses a fixed dollar amount throughout |

| Matches depreciation expense to actual asset value loss, giving a more accurate picture of true asset worth on your balance sheet | Unsuitable for assets that hold value evenly over time, such as buildings or land improvements, where applying DDB distorts financial statements |

| Aligns the asset’s highest expense period with its highest productivity period, which reflects the economic reality of most equipment and technology | Produces lower reported net income in early years, which can affect the financial ratios lenders and investors use to evaluate the business. Understanding how this interacts with your debt-to-capital ratio matters if you plan to raise funds. |

How to Calculate Double Declining Depreciation in Excel & Other Tools

You do not need to rebuild the formula from scratch each year. Excel has a built-in function that handles it automatically.

To build a depreciation schedule in Excel:

- Enter your asset’s original cost in a cell (for example, A2).

- Enter the salvage value in a cell below it (for example, A3).

- Enter the asset’s useful life in years (for example, A4).

- Use the formula

=DDB(cost, salvage, life, period), replacing each term with your cell references and the period number (1 for Year 1, 2 for Year 2, and so on). - Copy the formula down for each year of the asset’s life to build a complete schedule.

Excel automatically handles the Year 5 salvage adjustment. If you prefer a web-based calculator, several free tools produce the same results without any setup:

| Tool | Description | Cost | Best For |

|---|---|---|---|

| Calculator.net | Free online calculator supporting DDB and other methods with full schedule output | Free | Small business owners doing a quick check |

| Calculator Soup | Detailed step-by-step DDB schedule with exportable results | Free | Accountants who need to verify calculations |

| Omni Calculator | Fast DDB schedule on mobile and desktop with a clean interface | Free | Quick estimates on the go |

| Vedantu | Educational tool with worked examples alongside the results | Free | Learning the method for the first time |

Double Declining Balance in Financial Reporting: What GAAP & IFRS Require

Both Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) allow the double declining balance method, but both require that the method accurately reflect how the asset is actually used and worn down.

Choosing DDB purely to minimize taxes in a given year, without a genuine belief that the asset loses value rapidly, can create inconsistencies between your tax return and your audited financial statements.

On your income statement, DDB produces a higher depreciation expense in the early years. This directly reduces reported net income. On your balance sheet, the asset’s book value declines faster than under straight-line depreciation. Neither of these outcomes is a problem.

Both are accurate reflections of what is happening economically. The requirement under both GAAP and IFRS is simply that once you select a depreciation method for a class of assets, you apply it consistently and disclose it in your notes to financial statements.

For small businesses not subject to audit, the practical consideration is simpler: use whichever method matches how the asset actually loses value, and document your reasoning. That documentation matters if the IRS ever questions your depreciation deductions.

Common Mistakes That Cost Business Owners Money

A few errors keep occurring in depreciation calculations. Each one has real financial consequences.

Depreciating below the salvage value is the most common. The formula will keep producing a depreciation expense in Year 5 or Year 6, even when the book value is already at or near the salvage value. You must cap the final year’s deduction so the ending book value equals the salvage value exactly. Depreciating further can create an inaccurate book value on your balance sheet and overstate your tax deductions.

Applying the rate to the wrong base occurs when someone multiplies the depreciation rate by the original purchase price rather than the current book value. In Year 1, those numbers are the same. By Year 3, the gap is substantial. Always use the beginning book value for that specific year, which is the prior year’s ending book value.

Using DDB for assets that do not qualify is both an accounting error and a potential compliance issue. Land cannot be depreciated at all. Buildings typically fall under a 39-year straight-line depreciation schedule under MACRS. Applying DDB to these asset types misstates your financial position and may attract scrutiny during a tax audit.

Changing methods mid-asset without documentation causes confusion during audits and makes it difficult to reconstruct the asset’s full depreciation history. If you switch from DDB to straight-line partway through an asset’s life, which is permitted and often advantageous in later years, document the switch clearly in your records and note the book value at the time of the change.

Frequently Asked Questions

What is the double declining balance method?

The double declining balance method is an accelerated depreciation technique that applies twice the straight-line depreciation rate to an asset’s book value each year.

Because the book value decreases annually, the actual dollar amount expensed decreases each year, even though the rate remains fixed. The result is that most of the asset’s depreciation is captured in the first 2 or 3 years of ownership.

How do you calculate double declining balance depreciation step by step?

- First, determine the straight-line rate (1 divided by useful life) and double it.

- Second, multiply that rate by the asset’s book value at the start of the year.

- Third, subtract the result from the book value to get the ending book value.

- Fourth, repeat the process each year using the new ending book value as next year’s starting value.

Stop when the book value reaches the salvage value.

What is the difference between straight-line and double declining balance depreciation?

Straight-line depreciation spreads the cost evenly over the asset’s useful life, deducting the same dollar amount every year. Double-declining balance front-loads the deduction, expensing more in the early years and less later.

A straight-line method is simpler and produces more stable reported earnings. DDB better matches the actual value loss of assets like vehicles and computers, and reduces taxable income more quickly.

When should a business use the double declining balance method?

Use the double declining balance method when the asset loses a significant portion of its value in its first few years. Vehicles, computers, heavy equipment, and technology hardware are the clearest cases.

Avoid DDB for assets that hold their value evenly over time, such as commercial real estate or office furniture.

The method only makes sense when the front-loaded depreciation pattern matches what is actually happening to the asset’s market value.

Does the IRS allow double-declining balance depreciation?

Yes. The IRS uses double declining balance as the default method within the Modified Accelerated Cost Recovery System (MACRS) for most 3-year, 5-year, 7-year, and 10-year property.

IRS Publication 946 provides the full property class tables and depreciation percentages. If you are filing a U.S. business tax return, you are likely already using a DDB-based system for eligible assets without knowing it.

What happens when the book value reaches the salvage value in double declining balance?

Depreciation stops completely once the book value reaches the salvage value. In practice, the final year’s deduction must be reduced so the ending book value lands exactly at the salvage amount.

If the formula produces a depreciation figure that would push the book value below salvage, you cap the deduction at the difference between the current book value and the salvage value. Depreciating an asset below its salvage value is an accounting error.

Can you switch from double declining balance to straight-line depreciation mid-asset?

Yes, and it is often the right move. In later years, when the DDB formula produces a smaller deduction than straight-line would on the remaining book value, switching to straight-line maximizes your total deduction.

MACRS actually builds this switch in automatically. For financial reporting purposes, a mid-asset switch is permitted under GAAP but requires disclosure in your financial statements and consistent application going forward.