Need a smarter way to depreciate your business assets that lose value fast instead of spreading costs evenly over years? The double declining balance method lets you expense more upfront when assets like computers and vehicles are newest and most valuable.

I’ve simplified everything about this accelerated depreciation technique so you can understand when it makes sense for your business taxes.

You’ll discover how this approach differs from straight-line depreciation and why manufacturers and tech companies prefer it for equipment costs.

Understanding this method helps you make better financial decisions about asset management and maximize your early-year tax deductions legally.

Let me show you exactly how the double declining balance method works in plain language anyone can follow.

What is the Double Declining Balance Method?

The double declining balance method is an accounting technique that lets businesses expense assets faster in the early years of ownership.

It’s a type of accelerated depreciation method, meaning you write off more of an asset’s value upfront rather than spreading it evenly.

This approach doubles the rate you’d use with straight-line depreciation, hence the name “double declining” in the title of this method. Businesses use this when assets lose value quickly in their first few years, like computers, vehicles, or machinery that wears out.

The method helps companies reduce taxable income early on, improving cash flow when the asset is newest and most productive overall.

How Does the Double Declining Balance Method Work?

The double declining balance method accelerates depreciation by applying double the straight-line rate to a decreasing book value each year. I’ll break down the core principle and key formula components so you can calculate depreciation correctly for any asset:

Core Principle

The double declining balance method speeds up depreciation by applying twice the straight-line rate to an asset’s book value each year. Instead of spreading the cost evenly, it calculates depreciation based on a shrinking asset value.

This means more expense is recognized early on, reflecting assets losing value faster at the start of their use.

Each year, the book value declines, so applying double the straight-line rate results in smaller depreciation amounts over time.

This method suits assets that wear out or become obsolete quickly, giving a realistic expense pattern.

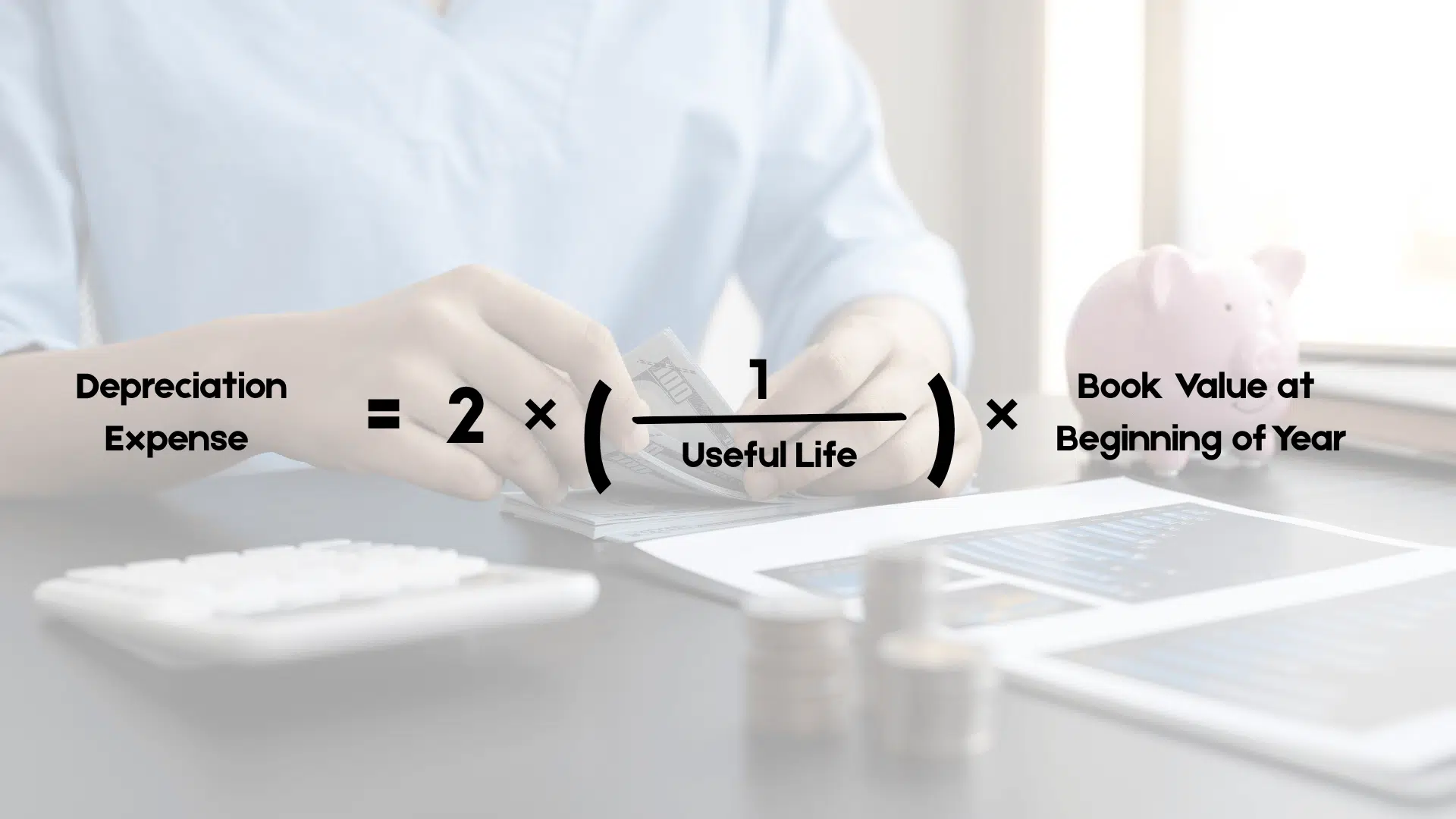

Formula and Components

Here are the key terms and values you need to understand before applying the double declining balance method to any asset. Knowing these components helps you calculate depreciation accurately and avoid common mistakes:

- Asset cost (purchase price): This is the original amount paid to buy the asset.

- Useful life (in years): How many years the asset is expected to be useful.

- Salvage value (residual worth at the end): Estimated value after the asset’s useful life.

- Depreciation rate (double the straight-line rate): Twice the rate of straight-line depreciation.

- Book value at the beginning of the year: Current asset value after subtracting depreciation so far.

These terms form the foundation of every double declining balance calculation you’ll perform throughout the asset’s useful life. Understanding each component ensures you can accurately track how much value your asset loses each year.

Double Declining Depreciation vs. Straight-Line Method

Understanding the differences between these two depreciation methods helps you choose the right approach for your specific assets and financial goals. Here’s how straight-line and double declining balance methods compare across key factors:

| Aspect | Straight-Line Method | Double Declining Balance Method |

|---|---|---|

| Depreciation Pattern | Equal expense every year | Higher early-year expense, lower later |

| Annual Expense | Same amount each period | Decreases each year |

| Calculation Basis | (Cost – Salvage Value) ÷ Useful Life | Book Value × (2 ÷ Useful Life) |

| Tax Benefit Timing | Spread evenly over the useful life | Front-loaded in early years |

| Best For | Stable-use assets like furniture, buildings | Assets that lose value quickly, like tech, vehicles, and machinery |

| Complexity | Simple, consistent calculations | More complex, changes annually |

| Cash Flow Impact | Steady tax deductions | Higher early tax savings |

| Book Value Decline | Linear, predictable | Rapid initial decline, slows over time |

Use Double Declining Balance for assets that lose value quickly, like technology and vehicles; use Straight-Line for stable assets like furniture and buildings.

Example of Double Declining Depreciation

Let’s walk through a real example using a $10,000 asset with a 5-year useful life and $1,000 salvage value. This table shows how depreciation expense decreases each year while the asset approaches its salvage value:

Asset Details:

- Purchase Price: $10,000

- Useful Life: 5 years

- Salvage Value: $1,000

- Depreciation Rate: 40% (2 ÷ 5 years)

| Year | Beginning Book Value | Depreciation Rate | Depreciation Expense | Ending Book Value |

|---|---|---|---|---|

| 1 | $10,000 | 40% | $4,000 | $6,000 |

| 2 | $6,000 | 40% | $2,400 | $3,600 |

| 3 | $3,600 | 40% | $1,440 | $2,160 |

| 4 | $2,160 | 40% | $864 | $1,296 |

| 5 | $1,296 | Adjusted | $296 | $1,000 |

Pattern Explanation: Notice how depreciation expense starts high at $4,000 in year one and decreases each subsequent year.

The final year requires an adjustment to $296 instead of the calculated $518 to ensure the ending book value matches the salvage value exactly. This pattern reflects how assets typically lose more value when they’re new and less as they age.

When to Use the Double Declining Balance Method

The double declining balance method works best for assets that lose value quickly during their first few years of use.

Vehicles, computers, smartphones, and technology equipment depreciate rapidly as newer models replace them almost immediately after purchase and deployment.

Industries with rapid innovation or heavy machinery often prefer this method because equipment becomes outdated or less efficient very quickly.

Manufacturing companies, construction firms, and tech businesses commonly use the double declining balance method for their expensive equipment and tools that wear out.

This method also helps with tax planning by allowing businesses to claim larger deductions early, reducing taxable income when cash flow matters most.

Use this approach when your asset will genuinely lose more value upfront rather than depreciating evenly over its entire lifespan.

Double Declining Balance Method: Advantages and Disadvantages

Understanding both the benefits and drawbacks of the double declining balance method helps you decide if it’s right for your business. Here’s how this depreciation approach compares in terms of advantages and potential limitations:

| Advantages | Disadvantages |

|---|---|

| Recover a larger portion of the asset’s cost in the early years when cash flow is critical for business operations | Requires annual recalculation based on changing book values instead of using a simple fixed amount each year |

| Aligns higher depreciation with periods when assets are most productive and generate the most value for the business | Inappropriate for assets that depreciate uniformly over time, like buildings, office furniture, or other stable equipment |

| Reduces taxable income significantly in early years, improving cash flow and lowering the overall tax burden immediately | Creates lower net income initially, which may negatively affect financial ratios and investor perceptions of company performance |

Weighing these pros and cons against your specific business needs and asset types ensures you choose the most beneficial depreciation method. The right choice depends on your cash flow priorities, tax strategy, and how your assets actually lose value over time.

How to Calculate Double Declining Depreciation?

Calculating double declining depreciation becomes much easier when you use the right tools instead of doing complex math by hand. I’ll show you how to use Excel’s built-in function and other free online calculators to automate your depreciation schedules:

Calculating Double Declining Depreciation in Excel

Excel provides a built-in DDB function that automates double-declining balance calculations and saves you time on manual math. Follow these simple steps to create an accurate depreciation schedule quickly:

- Enter your asset’s initial cost in a cell (e.g., A2).

- Enter the salvage value (estimated residual value) in another cell (e.g., A3).

- Enter the asset’s useful life (number of periods, usually years) in a cell (e.g., A4).

- Use the formula

=DDB(cost, salvage, life, period)where you replace these with your cells and the period number. - Copy the formula down for each depreciation period to build a full schedule.

With this method, you automate your depreciation table easily in Excel. It updates totals and handles complicated calculations. Now your depreciation tracking is fast and reliable.

Calculating Double Declining Depreciation Using Other Tools

Here are some helpful online tools and calculators that make double-declining balance depreciation calculations quick and accurate for everyone. These resources range from built-in Excel functions to free web-based calculators for different user needs:

| Tool Name | Description | Pricing | Integration Options | Best For |

|---|---|---|---|---|

| Calculator.net Depreciation Calculator | Free online calculator with DDB and other methods | Free | Web-based, no integration | Small business owners, students |

| Calculator Soup Depreciation Calculator | Free tool offering detailed DDB calculations stepwise | Free | Web-based, exportable results | Accountants needing quick checks |

| Omni Calculator Depreciation Tool | Intuitive calculator offering fast DDB schedules | Free | Mobile and desktop web access | Casual users, quick estimates |

| Vedantu Double Declining Calculator | Educational tool with accurate DDB results and examples | Free | Web-based | Students, accounting learners |

Each tool offers unique advantages depending on if you need integration with accounting software, mobile access, or educational examples. Choose based on your technical comfort level, if you need exportable results, and how often you’ll perform depreciation calculations.

Double Declining Balance in Financial Reporting and Tax

Double Declining Balance (DDB) shows up on income statements as higher depreciation expense early on, which lowers net income in those years. On balance sheets, the asset’s book value reduces faster compared to straight-line depreciation.

Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) both allow DDB for accelerated depreciation, but require clear disclosure.

For tax, the IRS uses the Modified Accelerated Cost Recovery System (MACRS), which often employs DDB or similar accelerated methods to help businesses reduce taxable income earlier.

This method matches the asset’s expense with its higher early usage, improving financial accuracy and offering tax deferral benefits for companies.

Double Declining Balance Method: Common Mistakes to Avoid

Even experienced accountants make errors when calculating double declining balance depreciation, so knowing what to watch for protects your financial records. Here are the most frequent mistakes people make and how you can avoid them in your own calculations:

- Forgetting to stop depreciation at salvage value can result in depreciating the asset below its residual worth, creating inaccurate financial statements.

- Misapplying the rate or using the wrong beginning value leads to incorrect depreciation amounts that compound errors throughout the asset’s useful life.

- Using it for non-depreciable assets like land violates accounting standards since land doesn’t lose value over time and shouldn’t be depreciated.

- Mixing methods midway without clear documentation creates confusion during audits and makes it impossible to track asset values accurately over time.

Avoiding these common pitfalls ensures your depreciation calculations remain accurate and compliant with accounting standards throughout the asset’s life. Double-check your work each year and maintain clear records of your depreciation method choices for every single asset.

Summing It Up

Mastering the double declining balance method gives you a powerful tool for managing asset depreciation and improving early-year cash flow. I hope this breakdown showed you when to use this accelerated approach versus simpler methods for different asset types.

Remember that front-loading depreciation makes perfect sense for technology and vehicles but creates unnecessary complexity for stable assets like furniture.

Your accounting software or Excel can automate most calculations once you understand the basic principles and formula behind this method.

Always verify you’re stopping at salvage value and maintaining consistent records throughout each asset’s useful life for accurate reporting.

What asset in your business would benefit most from accelerated depreciation right now? Share your depreciation challenges in the comments below.