Let me be honest with you: budgeting isn’t about punishment or restriction. It’s simply a plan for my money, and once I understood that, everything shifted.

Think of it as creating a roadmap that shows where my income goes each month. Without one, I’m essentially wandering around hoping things work out.

What makes a budget truly successful goes beyond just saving money. It’s about tracking my actual spending patterns, planning for what’s ahead, and ensuring my financial choices align with what genuinely matters to me.

Throughout this guide, I’ll walk you through the essential components that make budgets work, share practical tips that have helped me stay on track, and point out the common mistakes that trip people up so you can avoid them entirely.

What is a Budget and Why Does it Matter?

A budget is simply telling my money where to go instead of wondering where it went. It’s my financial game plan that assigns every dollar a job before the month begins.

Why does this matter? Because budgeting is my foundation for:

- Financial Stability: I know exactly what’s coming in and going out.

- Debt Reduction: I can intentionally direct extra funds toward what I owe.

- Goal Achievement: Whether it’s a vacation or retirement, I’m actively working toward it.

Here’s the reality: nearly two-thirds of Americans don’t follow a formal budget, which explains why so many feel financially stressed. Let’s break down the key components that make a budget truly successful.

Key Components of Successful Budgeting

A budget isn’t a single spreadsheet I set up and forget about. It’s built from several moving parts that work together to keep my finances healthy and my goals within reach.

Overly rigid budgets lead to abandonment, while ignoring emergency savings leaves me vulnerable to debt spirals. High-interest debt compounds rapidly, and delaying investments costs years of growth. Balance immediate protection with long-term security.

1. Clear Financial Goals

Without knowing what I’m working toward, my budget becomes just a list of restrictions. I need both short-term goals, like saving for a vacation or building my emergency fund, and long-term ones, like paying off student loans or saving for a down payment.

These goals give every dollar I save actual purpose and make sticking to my budget feel worthwhile rather than restrictive.

Actionable Tip: Write down three financial goals and assign target dates to each one. This transforms vague wishes into concrete objectives to budget for.

2. Accurate Income Tracking

I need to know precisely how much money flows into my accounts each month. This means tracking my salary, freelance payments, side hustle earnings, rental income, or any other source.

The key is focusing on after-tax income, which actually hits my bank account, because that’s the real money I have to work with when allocating funds.

Actionable Tip: Calculate monthly take-home pay by reviewing the last three pay stubs and averaging them if income fluctuates.

3. Categorized Expenses

Breaking my spending into categories helps me see exactly where my money goes. I separate fixed expenses like rent, insurance, and car payments from variable ones like groceries, dining out, and entertainment.

This categorization reveals patterns I might otherwise miss, like realizing I spend more on subscriptions than I thought, and shows me where I have flexibility to adjust.

Actionable Tip: Review last month’s bank statements and sort every expense into either fixed or variable categories using a simple spreadsheet.

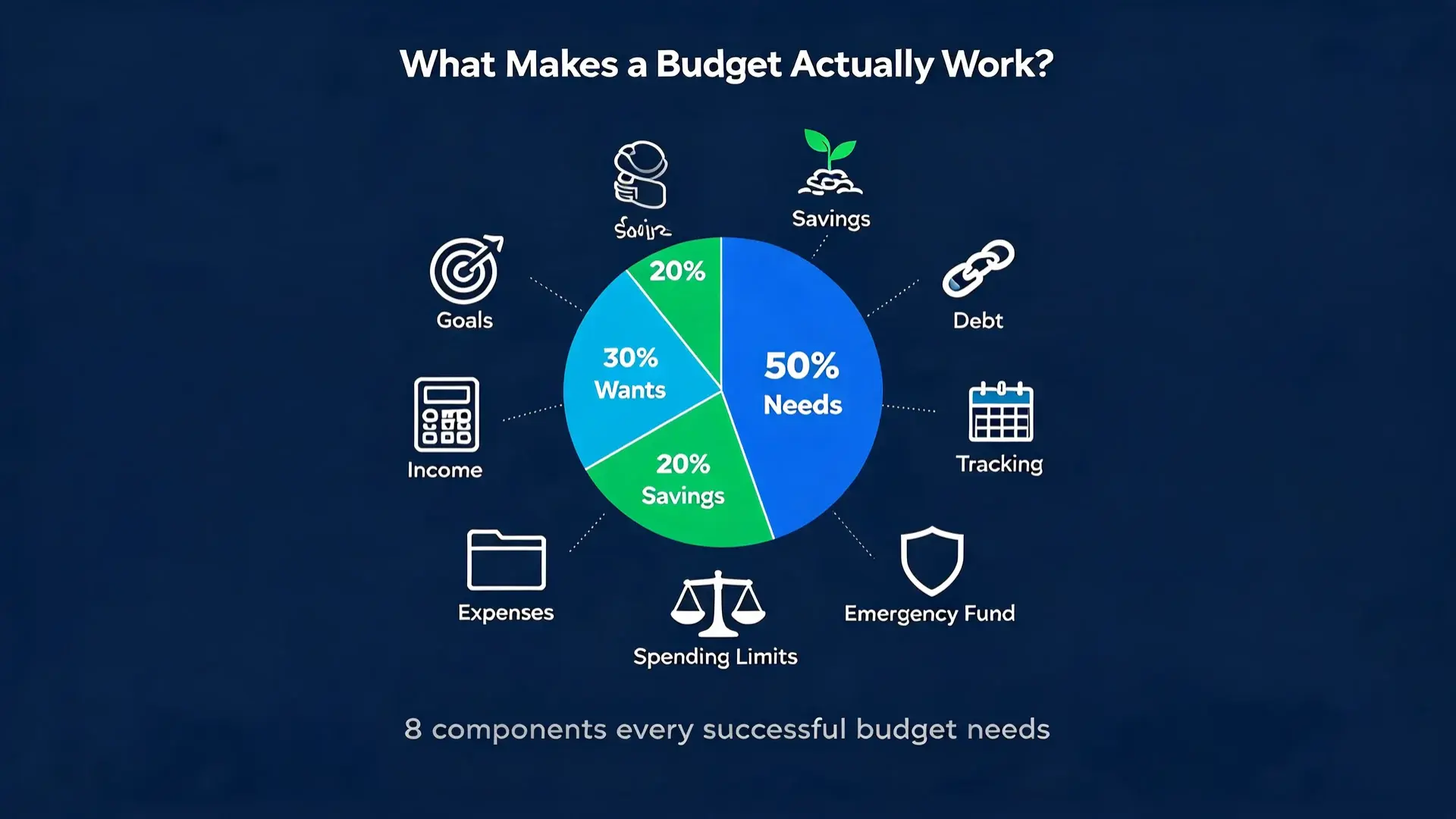

4. Realistic Spending Limits

Setting limits that are too strict sets me up for failure and burnout. I need boundaries that feel sustainable long-term, not like I’m punishing myself.

The 50/30/20 rule offers a helpful starting point: allocating 50% of income to needs, 30% to wants, and 20% to savings. I can adjust these percentages based on my situation and priorities.

Actionable Tip: Start with current spending habits and reduce gradually rather than making drastic cuts that won’t last.

5. Emergency Fund Allocation

Life throws curveballs: unexpected car repairs, medical bills, and job loss can all hit without warning. Without an emergency fund, these situations derail my entire budget.

I aim to save three to six months of living expenses in an easily accessible account. This safety net transforms potential financial disasters into manageable inconveniences and gives me genuine peace of mind.

Actionable Tip: Automate a weekly or biweekly transfer of even a small amount into a separate savings account dedicated solely to emergencies.

6. Regular Tracking and Adjustments

Creating a budget once isn’t enough; I need to check in regularly to see how I’m actually doing. Monthly reviews let me compare what I planned to spend against what I actually spent.

My income changes, prices increase, and new priorities emerge, so my budget needs to evolve accordingly rather than becoming outdated and irrelevant.

Actionable Tip: Set a recurring calendar reminder on the last day of each month to review spending and make necessary adjustments for the upcoming month.

7. Debt Management Strategy

Ignoring my debt doesn’t make it disappear, so I integrate payments directly into my budget. Using either the snowball method for quick wins or the avalanche method to save money, having a clear strategy keeps me motivated. Managing debt strategically frees up cash flow over time for other goals.

Actionable Tip: List all debts with their interest rates and minimum payments, then choose one method and add extra payments to the budget for the target debt.

8. Savings and Investments

Budgeting isn’t only about controlling spending; it’s about building wealth for my future. I include categories for retirement contributions, education funds, and investing for beginners alongside my emergency savings.

Treating savings as a non-negotiable expense rather than whatever’s left over ensures I’m consistently working toward financial security and growth.

Actionable Tip: Increase retirement contributions by just 1% and automate it. The difference will barely be noticeable in your paycheck, but the long-term impact is substantial.

Tools and Methods to Simplify Budgeting

Proven methods and modern tools already exist to make budgeting manageable. The right combination can turn this from a chore into something surprisingly straightforward.

| Tool/Method | What It Is | Best For |

|---|---|---|

| Zero-Based Budgeting | Assign every dollar a job until income minus expenses equals zero | Complete control over every dollar |

| Envelope System | Allocate cash into physical or digital envelopes per category | Curbing overspending in specific areas |

| 50/30/20 Method | Split income: 50% needs, 30% wants, 20% savings | Simple framework for beginners |

| Mint | Free automated tracking and categorization | Hands-off, automated budgeting |

| YNAB | Zero-based app with goal tracking (subscription-based) | Serious budgeters wanting detailed control |

| EveryDollar | User-friendly drag-and-drop interface | Simplicity without complexity |

| Google Sheets | Customizable spreadsheet templates | Full customization and manual control |

These digital tools sync bank accounts, categorize transactions instantly, and provide visual spending insights. What once took hours of manual work now happens in real-time, letting me focus on smart decisions rather than number-crunching.

When linking bank accounts to budgeting apps, ensure they use bank-level encryption and two-factor authentication. Protect financial data as carefully as the money itself.

Common Budgeting Mistakes to Avoid

Even with the best intentions, it’s easy to fall into traps that derail an otherwise solid budget. Recognizing these common mistakes helps me steer clear of them before they become problems.

- Ignoring Irregular Expenses: Annual subscriptions, holiday gifts, and quarterly insurance payments are easy to forget until they suddenly land and leave me short.

- Setting Unrealistic Goals or Limits: Overly restrictive budgets leave no room for life, leading to burnout and abandoned plans within weeks.

- Forgetting to Track Small Purchases: Daily coffee runs and impulse buys seem harmless individually, but they can quietly drain hundreds from a budget each month.

- Not Revisiting the Budget After Major Life Changes: Using the same budget after a raise, a move, or a new baby makes it completely irrelevant to the current reality.

When I recognize these patterns early, I can course-correct before they undermine all the progress I’ve made.

Benefits of Successful Budgeting

Budgeting isn’t just about restriction; it’s about building genuine financial freedom. Here’s what happens when I commit to managing my money intentionally.

1. Reduces Financial Stress and Anxiety

There’s something profoundly calming about knowing exactly where I stand financially. When I have a budget, those middle-of-the-night worries about whether I can cover next month’s bills fade away.

I’m not constantly checking my bank balance with dread or avoiding looking at my accounts altogether. Instead, I feel grounded because I have a plan, and that plan removes the uncertainty that fuels financial anxiety.

2. Helps Achieve Both Short-Term and Long-Term Goals

A budget turns my dreams into actionable steps. Whether I’m saving for a weekend getaway next month or a down payment in five years, my budget shows me exactly how much to set aside and when I’ll reach each milestone.

Without it, goals remain wishful thinking. With it, I’m making measurable progress every single month, watching those targets get closer and feeling motivated to keep going.

3. Builds Better Credit and Long-Term Wealth

When I budget properly, I pay bills on time, keep credit utilization low, and avoid debt traps, all of which boost my credit score. Beyond that, consistently directing money toward savings and investments compounds over time.

What starts as small monthly contributions grows into substantial wealth. Budgeting isn’t just about managing today’s money; it’s about building the financial foundation for decades to come.

4. Creates a Sense of Financial Confidence and Control

Nothing beats the feeling of being in the driver’s seat of my financial life. Budgeting gives me that control; I decide where my money goes instead of wondering where it went.

This confidence spills into other areas of my life, making me feel more capable and empowered, which is one of the broader financial literacy skills that budgeting quietly builds over time. I’m not at the mercy of my finances anymore; I’m actively shaping my financial future with every decision I make.

How to Stay Consistent with Your Budgeting

Creating a budget is one thing; sticking to it month after month is where the real challenge lies. Here’s how I keep myself on track without feeling deprived or overwhelmed:

- Schedule Monthly Budget Reviews: I block out time on the last day of each month to assess what worked, what didn’t, and what needs adjusting going forward.

- Reward Yourself for Hitting Financial Milestones: I celebrate when I reach savings goals or pay off debt with small, meaningful treats that don’t derail my progress.

- Keep Goals Visible: I use vision boards, phone reminders, or notes on my mirror to keep my financial targets front and center every single day.

- Stay Flexible: I treat my budget as a living document that adapts to life changes, unexpected expenses, and shifting priorities rather than a rigid rulebook.

- Automate What You Can: I set up automatic transfers for savings and bill payments so consistency happens without relying solely on willpower or memory.

Consistency doesn’t mean perfection; it means showing up for my budget regularly and making small adjustments as life unfolds. The more I practice these habits, the more natural budgeting becomes.

Frequently Asked Questions About Budgeting

What is the 50/30/20 rule, and does it actually work?

The 50/30/20 rule divides after-tax income into three buckets: 50% for needs like rent, utilities, and groceries; 30% for wants like dining out and entertainment; and 20% for savings and debt repayment.

It works well as a starting framework because it’s simple enough to follow without a finance background and flexible enough to adjust based on individual circumstances. That said, it won’t suit everyone.

What is the difference between the snowball and avalanche debt payoff methods?

The snowball method focuses on paying off the smallest debt balances first while making minimum payments on everything else. As each small balance is cleared, the freed-up payment gets rolled into the next one, building momentum.

The avalanche method prioritizes the debts with the highest interest rates first, which saves more money overall because high-interest debt grows the fastest.

Is budgeting worth it if my income is irregular?

Budgeting is actually more important with an irregular income, not less. The most effective approach for variable income is to base the budget on the lowest average monthly income from the past three to six months, treating any income above that floor as a bonus to direct toward savings or debt.

This creates a buffer that makes the unpredictable months manageable. Apps like YNAB were specifically designed with irregular earners in mind and can make this process considerably more structured.

The Bottom Line

Here’s what I know for certain: a successful budget isn’t complicated. It’s simply balancing what comes in with what goes out, while keeping my goals in sight through regular tracking and honest planning.

Perfection isn’t the goal; consistency is. Missing a day or overspending one week doesn’t mean failure; it means I’m human.

The real power comes from showing up repeatedly, adjusting as needed, and refusing to give up on myself. If you’re ready to take control, start small. Track just one week of spending. Notice where your money actually goes.

That single step creates momentum, and momentum creates change. What’s holding you back from starting today?